Saskatchewan Wildfire Insurance Claims: Step-by-Step

The escalating catastrophe landscape of recent years, culminating in Canada’s second-largest wildfire season on record in 2025, where roughly 8.9 million hectares burned and over 75,000 citizens faced mandatory displacement, has fundamentally repositioned how the insurance sector values wildfire exposure.

With exposure climbing across the country, staying ahead of seasonal risks is crucial.

The 2026 Wildfire Landscape: Coast-to-Coast Risk

As we approach the critical summer months of 2026, emergency response units and provincial authorities are aggressively realigning their strategies to counter early structural and climate signals.

⚠️

Critical Exposure: Data from Intact Financial Corporation shows that 61% of Canadians remain largely relaxed or unconcerned about their personal wildfire risk.

This is a staggering psychological gap, considering that 60% of all Canadian communities are structurally located within areas that intermingle with volatile forest fuels.

💡

Modern Mitigation Realities: Airborne embers can travel an average of two km from the main fire front to ignite debris in unprotected gutters, yards, etc.

As highlighted by aerial firefighting strategies, if your property falls within a high-risk zone, localized structural resilience through FireSmart adjustments (see end of article for a list) is your primary line of defence.

Regina Climate Projections & Wildfire Vulnerability

In the near future, these dangerously hot days are projected to become an annual occurrence. Data from across the country indicate that climate shifts significantly alter seasonal metrics, influencing what might be considered overall wildfire risk profiles for cities.

The table below outlines the custom data parameters for the Regina zone:

📱Note for mobile users: Scroll left or swipe across the table below to view all columns and information.

| Climate Metric (Regina Region) | Historical Baseline | 2021-2050 (Low Carbon RCP4.5) | 2021-2050 (High Carbon RCP8.5) |

|---|---|---|---|

| Mean Annual Temperature | 2.9°C | 4.7°C | 5.2°C |

| Days with Max Temp > 30°C | 11.8 Days | 21.0 Days | 24.3 Days |

| Days with Max Temp > 34°C | 2.6 Days | 5.8 Days | 7.2 Days |

| Very Hot Days (Max Temp > 38°C) | 0.3 Days | 1.0 Days | 1.4 Days |

| Frost Days (Min Temp < 0°C) | 182.2 Days | 160.8 Days | 155.0 Days |

Data Note: Projections derived from the Climate Atlas of Canada. The sharp escalation in days exceeding 30°C directly correlates with severe evapotranspiration, stripping moisture from ground fuels and radically inflating seasonal fire weather ratings.

When you combine a longer frost-free season with a massive spike in days over 30°C, it triggers a process called severe evapotranspiration. Essentially, the extreme heat acts like a giant sponge, rapidly sucking moisture out of the soil, grass, brush, and trees.

Because the ground fuels are stripped of their moisture much faster than they used to be, the overall “fire weather” ratings shoot up. This environment creates a landscape where wildfires are much easier to ignite and significantly harder for emergency crews to contain.

How Wildfire Rules Change for Different Types of Properties

Your coverage limits and payout rules depend entirely on how insurance companies categorize your property:

🏠

1. Standard Home Insurance

Coverage Caps: Personal liability protection starts at $1,000,000 but can go up to $5,000,000.

Your Share of Costs: Your deductible, the initial amount you pay out of pocket before insurance covers the rest.

Guaranteed Replacement Cost (GRC): If your home was built after 1960 and has 100-amp power, you may qualify for Guaranteed Replacement Cost. This means the insurer pays to completely rebuild your home, even if the cost exceeds your policy limit.

🔑

2. Renter Insurance

Coverage Caps: You can protect your belongings for up to $200,000 (or as little as $30,000).

Your Share of Costs: Your deductible, the initial amount you pay out of pocket before insurance covers the rest.

🌲

3. Cabins & Vacation Homes

Coverage Caps: Maximum protection limits can reach $500,000 near fire hydrants, but are limited to $250,000 in unprotected areas (coverage follows the amount listed on the policy).

Age Penalty: If your cabin is over 10 years old (and Replacement Coverage (RC) is NOT listed), payouts are based on Actual Cash Value. This means the insurer subtracts wear and tear from your payout instead of giving you the amount a brand-new item costs today.

Pro Tip: To avoid the age penalty and potentially get replacement value, your cabin must be built after 1980, be fully open to vehicles year-round, sit on a permanent concrete foundation, and use a primary heat source other than wood or oil.

🚜

4. Farm Outbuildings & Fences

Blanketed (Non-Scheduled) Buildings: Any outbuildings originally designed or historically used for farming or business are automatically covered under a general “blanket” up to a strict cap. You do not have to list these individually, but they share that single, small pool of money.

Scheduled Buildings: This means listing the building separately on your policy with its own dedicated dollar limit and submitting recent photos. Scheduled buildings require an extra premium.

How Fences Work: Fences on your primary property lines are considered detached structures and use your standard (Detached Private Structures) limit. However, if you have extensive fencing or a fence on a separate piece of land away from the main site, it must be explicitly scheduled in your policy to be covered.

How Your Coverage Works:

If a wildfire damages your property, your insurance payout is split into a few main categories. Here’s a breakdown to help you know exactly where your coverage is coming from:

📱Note for mobile users: Scroll left or swipe across the table below to view all columns and information.

| What’s Covered | What It Pays For | Payout Limits | Important Rules |

|---|---|---|---|

| 🏠 Your House & Outbuildings | Pays to repair or rebuild your main home and other structures on your land, like detached garages or tool sheds. | Up to your total policy dollar limit, unless you qualify for full replacement cost (farm buildings differ). | Coverage Freeze: You cannot buy a new policy or increase your limits if your area is under an active evacuation order or if a wildfire gets within 50 kilometres of your property. |

| 💎 Your Belongings (Contents) | Pays to replace the items inside your home, from furniture to clothes and electronics. | Limited to the overall amount of content coverage stated on your policy. | The Scheduling Rule: Separately scheduled items are limited to the value stated on the policy, while unscheduled items might only receive actual cash value. |

| 🏨 Additional Living Expenses (ALE) | Helps pay for the extra day-to-day costs you face if you can’t live in your home because of fire or smoke damage. | Limited to the amount stated on your policy. | Must be carefully tracked. Save every single receipt and talk directly with your claims adjuster to manage these payouts. |

| 🚨 Mass Evacuation Protection | Provides immediate emergency money for lodging, fuel, and food if you are ordered out of your neighbourhood. | The amount of time this coverage lasts can vary. | Kicks in automatically the moment local civil officials issue a mandatory evacuation order because a wildfire is heading your way. |

| 🚒 Fire Department Charges | Reimburses you if a local municipal fire team or volunteer brigade bills you for coming out to protect your home. | A base protective limit of $20,000 is typically included across all standard SGI CANADA personal property products. | You can pay a little extra to raise the coverage limit before a seasonal threat begins. |

| 🌲 Prairie & Forest Fire Fighting | Covers specialized expenses and active resource costs tied to fighting a spreading brush, grass, or forest fire that threatens your property line. | Subject to specific policy category allocations and regional group underwriting limits. | Designed to cover the broader logistics, tools, and local fire line suppression measures used to stop a wildfire front from reaching your buildings. |

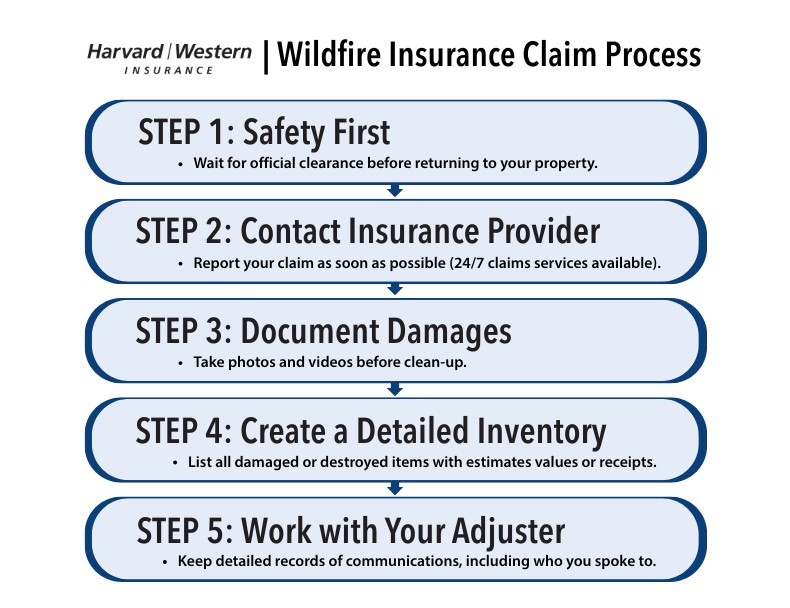

How to File a Fire Loss Claim

If your property is impacted by a wildfire event, initiate the standard claims protocol immediately:

Contact Your Broker Immediately:

Access the 24-hour emergency intake claim lines to activate your file. Provide detailed structural notes, your active temporary contact information, and your emergency location details.

Request an ALE Advance:

If you are displaced by an evacuation or if your home is unlivable, request an immediate allocation for Additional Living Expenses to maintain cash flow for emergency lodging and food.

🚨

Wait for Official Clearances: Never attempt to re-enter a fire zone until emergency response teams and civil authorities issue an official, unconditional “All Clear” notice.

Proof of Loss Protocols

To secure a complete, equitable settlement following a wildfire loss event, precise asset tracking is mandatory. The claims department requires clear documentation to confirm values before processing payouts.

📋Documenting Wildfire Damages

STEP 1

📸

Take Photos & Video

Capture detailed visual evidence of everything. Document the damage to your home from multiple angles, landscape impacts, and individual interior belongings before cleaning up or moving items.

STEP 2

📝

Create a Detailed List

Write down descriptions of all damaged or destroyed items. Group them by room and include details like the approximate purchase year, brand names, model numbers, and replacement values.

STEP 3

💵

Keep Receipts & Logs

Save every single receipt for your temporary living costs, including hotels, meals, and fuel. Maintain a written log of dates, times, and summaries of conversations with your adjuster.

📝

Advisory Note: If records are completely lost due to a fire, do not panic. Insurers have structured processes for tracking missing documentation. Your claims adjuster will provide standard loss declaration forms to help rebuild your asset profile safely.

Resources from FireSmart™ Canada

If you haven’t yet, check out FireSmart Canada. They have great programs designed to help neighbourhoods become more resilient to wildfires.

→ They offer a free one-hour course called FireSmart 101 that’s full of practical tips for protecting your home.

What are the best ways to lower your wildfire risk?

- Move things like firewood or propane tanks at least 30 feet away from your house and any sheds.

- Nothing flammable should be touching your siding, deck, or porch.

- Keep your grass cut short (under 10 cm) to slow down approaching flames.

- Try to clear a “safety zone” by raking away mulch or dead leaves within five feet of your home.

Stay Connected With Harvard Western

Thanks for reading our article; I hope you enjoyed this month’s wildfire insurance claims topic. Here are some more ways to access more insurance information and tips:

1.

Visit our Blog/article page each month, where we publish various insurance articles and share information on specific industry products.

2.

Learn more about Claims and visit our support page for comprehensive information.

3.

Follow us on LinkedIn to stay up to date on our latest company updates.

Disclaimer: This article is provided for general informational purposes only and does not constitute formal legal or insurance advice. The information and guidelines outlined above are based specifically on SGI Canada underwriting manuals and policies. Please note that policy coverages, limits, and exclusions can vary significantly among different insurance companies. In all cases of discrepancy, ambiguity, or conflict regarding specific coverage terms, the official insurance policy wordings and documentation of your actual insurer will strictly prevail. Always consult directly with a licensed insurance advisor or broker to review your individual policy details.

Last updated:

Posted in Farm, Home & Tenant on May 29, 2025 by Hope Prost

Share:

Tweet